Economics begins with the idea of scarcity —

humans have virtually unlimited wants but resources (time,

labour, land and capital) are limited. Because we can’t

have everything we want, individuals and societies must

decide what to produce, how to produce it and for whom.

These decisions involve trade‑offs. The

opportunity cost of any choice is the value of

the next best alternative that is given up. For example,

if a student spends time studying economics instead of working,

the foregone wages are part of the opportunity cost. Recognising

opportunity costs helps people make better decisions about

resource use. Real‑world events underscore these concepts:

during the COVID‑19 pandemic, shortages of ventilators and protective equipment

forced governments to allocate limited supplies to hospitals, and

semiconductor shortages constrained automobile and smartphone production

worldwide. In everyday life, choosing to spend money on a night out may

mean delaying the purchase of new shoes. Scarcity and choice are

therefore at the heart of economic reasoning.

Factors of Production and Production Possibilities

Economists categorise inputs into four

factors of production: land (natural

resources), labour (human effort), capital (machinery,

tools and buildings) and entrepreneurship (the ability to

organise and innovate). Some economists also emphasise

human capital—the skills and education embodied in the

workforce—as a key factor. Each factor earns income:

land earns rent, labour earns wages, capital earns

interest and entrepreneurs earn profits. To illustrate

the trade‑offs society faces, economists use a

production possibilities curve (PPC), sometimes called

the production possibilities frontier. It plots the

maximum output combinations of two goods that can be

produced with a fixed set of resources and technology. Points

on the curve are efficient; points inside represent

under‑utilised resources (such as unemployment), while

points outside are unattainable without more resources or

better technology. When resources or technology improve—

for example, when a country invests in education or

develops better machinery—the PPC shifts outward. A

classic example pits “guns” (defence goods) against

“butter” (consumer goods): allocating more resources to

defence reduces the output of consumer goods, and vice

versa. Over time, increases in the labour force, capital

investment and technological progress allow economies to

produce more of both goods, effectively expanding the

frontier.

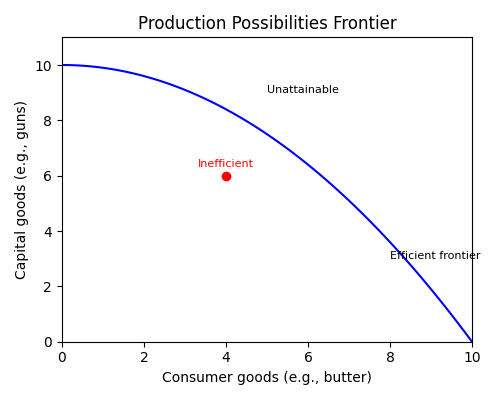

The Production Possibilities Frontier (PPF) illustrates the

trade‑off between two types of goods—in this case,

consumer goods and capital goods. Points on the curve are

efficient; the red dot inside the curve shows an

inefficient combination, while points beyond the curve are

unattainable without more resources or better technology.

Supply, Demand and Market Equilibrium

Supply and demand describe how prices are

determined in a market. Demand reflects the quantities

consumers are willing to buy at different prices; the

demand curve slopes downward because people buy more

when prices are lower. Supply reflects the quantities

producers are willing to sell; the supply curve

slopes upward because firms produce more when prices are

higher. The price at which quantity supplied equals

quantity demanded is the equilibrium price.

If the price is above equilibrium, excess supply leads

sellers to lower prices; if it’s below, shortages push

prices up. Changes in factors such as income, technology

or input costs shift the curves and create a new

equilibrium. For example, a drought that reduces the

harvest of corn shifts the supply curve to the left and

raises the equilibrium price, while rising household

incomes shift the demand curve for restaurant meals to

the right and increase both price and quantity. The

figure below illustrates a simplified supply‑and‑demand

diagram.

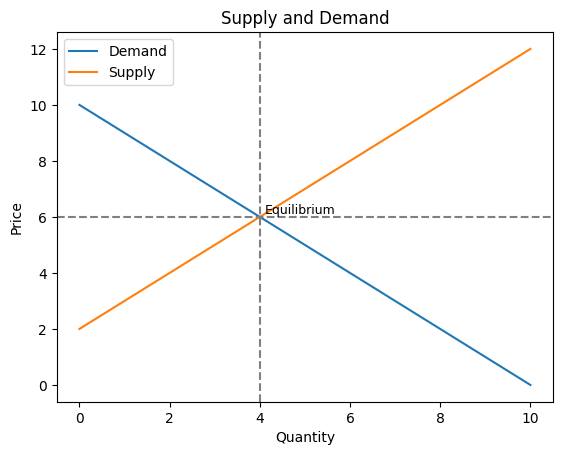

A simplified supply‑and‑demand diagram shows the downward‑sloping demand curve and the

upward‑sloping supply curve. The intersection (marked by dashed lines) represents the

equilibrium price and quantity where the market clears.

Gross Domestic Product (GDP)

Gross Domestic Product is the market value of

all final goods and services produced within a country’s

borders in a given period. Economists track the

percentage change in GDP from one quarter or year to the

next as a barometer of economic health. To make

comparisons over time, analysts adjust for changes in

prices: real or chained GDP removes the effects of

inflation and shows changes in actual output. Policymakers

use GDP data to set spending and tax policy, businesses use

it to plan investment and production, and individuals look

to GDP growth to gauge job prospects.

Economic growth is uneven. After the severe 2008–09

financial crisis, the U.S. economy entered its longest

expansion on record, lasting from June 2009 through

February 2020. Real GDP grew by roughly 2–3 % per year,

unemployment declined and corporate profits rose.

In early 2020 the COVID‑19 pandemic brought a

sudden halt to activity: real GDP contracted at an

annualised rate of about 32 % in the second quarter, and

the unemployment rate shot up to 14.7 %. Massive

fiscal stimulus and easy monetary policy helped fuel a

swift rebound. The chart below illustrates an index of

real GDP over time, with noticeable dips during the 2008–09

recession and the 2020 pandemic.

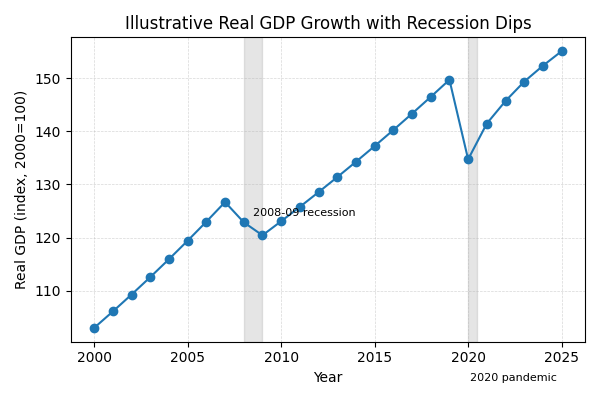

An illustrative real GDP index (base year 2000 = 100) shows

steady growth interrupted by recessions. The shaded

areas highlight the 2008–09 financial crisis and the

2020 pandemic, when GDP contracted sharply before

recovering.

Inflation and Purchasing Power

Inflation refers to a general, sustained increase in the

prices of goods and services across the economy, not just

isolated changes in the price of one product. When

inflation rises, the purchasing power of money declines:

each dollar buys fewer groceries, bus rides or textbooks.

Central banks target low and stable inflation (around 2 %

per year in the U.S. and euro area) because very high

inflation can disrupt economic planning and erode savings,

while deflation (falling prices) may discourage

consumption and investment.

In the 1970s, oil price shocks and expansive monetary

policy pushed inflation into double‑digit territory in many

countries, leading to stagflation—high inflation and high

unemployment. More recently, from mid‑2021 through 2022,

global supply‑chain snarls, a rebound in energy demand and

fiscal stimulus measures drove U.S. inflation to its

highest pace in four decades. Consumer prices rose

roughly 9 % year‑on‑year in June 2022, far above the

Federal Reserve’s goal, prompting aggressive interest rate

hikes. According to the Bureau of Labor Statistics, the

purchasing power of the dollar fell about 7.4 % between

2021 and 2022. These episodes underscore why savers need

to invest in assets that can outpace inflation over the

long term; holding cash alone means your money slowly

loses value.

Unemployment

A person is officially classified as unemployed if

they are jobless, have actively looked for work in the

past four weeks and are available to start a job. The

unemployment rate equals the number of unemployed divided

by the labour force (the employed plus the unemployed).

Economists also monitor broader measures of labour

underutilisation, such as the U‑6 rate, which adds

discouraged workers who have stopped looking for jobs and

part‑time workers who want full‑time hours.

High unemployment means the economy is operating below its

potential output—factories sit idle and families face

hardship. Very low unemployment can lead to labour

shortages and wage inflation. Historical data provide

perspective: during the Great Depression of the 1930s,

unemployment in the U.S. approached 25 %, while in the

early 2000s it hovered around 4 %. In April 2020,

lockdowns to slow the spread of COVID‑19 caused the U.S.

unemployment rate to spike to 14.7 %, the highest since

the Depression, before falling as businesses reopened.

Monetary Policy

Monetary policy is conducted by a country’s

central bank to influence the availability and cost of

money and credit. The key goal is to promote stable

prices and sustainable economic growth. Central banks

adjust short‑term interest rates, buy or sell government

securities, change reserve requirements for banks and

communicate future policy plans to steer expectations.

Lowering interest rates and expanding the money supply

make borrowing cheaper and encourage spending on homes,

cars and business investment; raising rates does the

opposite. Since 2008, central banks have supplemented

traditional tools with quantitative easing—buying

longer‑term assets to push down long‑term yields and

stimulate the economy.

Monetary policy actions have been front‑page news in recent

years. During the global financial crisis of 2008–09,

the U.S. Federal Reserve cut the federal funds rate to

nearly zero, purchased trillions of dollars of Treasury

and mortgage‑backed securities and used forward guidance to

reassure markets. In 2020, as the pandemic unfolded, the

Fed again slashed rates to zero and launched emergency

lending programs to keep credit flowing. Beginning in

2022, faced with the fastest inflation in decades, the

central bank pivoted and raised rates at the most rapid

pace since the 1980s. Other central banks, such as the

European Central Bank and the Bank of England, have used

similar tools to manage inflation and support growth.

Policymakers must walk a fine line: acting too slowly

risks runaway inflation, while tightening too quickly can

trigger recession.

Fiscal Policy

Fiscal policy involves the government’s choices

regarding taxation and public spending to influence

economic activity. Unlike monetary policy, which is

executed by independent central banks, fiscal policy is

determined by elected officials. During a recession,

governments often use countercyclical policy—cutting

taxes and increasing spending on public works, social

programs and unemployment benefits—to stimulate demand.

Conversely, during booms they may raise taxes or cut

spending to cool the economy and reduce public debt.

Real‑world examples abound. In the wake of the 2008

financial crisis, the U.S. enacted the American Recovery

and Reinvestment Act, a roughly $800 billion package of

tax cuts, infrastructure projects and aid to state

governments. During the pandemic, the CARES Act and

subsequent bills injected more than $5 trillion into the

economy through direct checks to households, expanded

unemployment insurance and loans to businesses. Other

countries implemented similar stimulus measures. Fiscal

policy can also be used to address long‑term challenges:

investments in education, healthcare and clean energy can

boost productivity and growth, while tax reforms can

encourage or discourage certain behaviours. Because

fiscal decisions involve trade‑offs (higher taxes, more

debt or fewer services), debates over the size and scope

of government are central to economic policy.

Interest Rates

An interest rate expresses the price of money. When you borrow, it is

the percentage of the principal you must pay in addition to repaying the amount borrowed. When you

save, it represents the return you receive on your deposit. Nominal rates are the quoted rates you

see on loans and savings accounts; real rates subtract inflation. Higher interest rates make

borrowing more expensive and encourage saving, while lower rates do the opposite.

Interest rates ripple through the economy. The U.S.

Federal Reserve sets a target range for the federal funds

rate, and banks base their prime lending rates on this

benchmark. When the Fed raises rates, credit card and

auto‑loan rates tend to increase, and mortgage rates often

follow suit; a one‑percentage‑point rise in the 30‑year

mortgage rate can boost the monthly payment on a $300,000

loan by several hundred dollars. Higher rates also

increase the cost of financing business investment, which

can slow corporate spending and hiring. Conversely,

lowering rates makes it cheaper to refinance a mortgage or

invest in a new factory and can stimulate consumption and

expansion. In 2020, for example, central banks slashed

rates to historic lows to cushion the pandemic’s blow; in

2022–23 they hiked rates aggressively to combat surging

inflation.

Externalities and Public Goods

Not all costs and benefits of economic activity show up in market prices. An externality

exists when a person’s or firm’s actions affect bystanders who are not part of the transaction. A

factory that emits smoke imposes health costs on nearby residents—a negative externality. On

the positive side, a homeowner who plants flowers attracts bees that pollinate neighbouring

orchards—a positive externality. Because polluters do not bear the full social costs and

innovators do not capture all the benefits of their ideas, markets on their own tend to overproduce

goods with negative externalities (like carbon emissions) and underproduce goods with positive

externalities (like basic research or vaccinations).

Public goods are goods that are nonrival (your use does not reduce someone else’s

enjoyment) and nonexcludable (it is difficult or impossible to prevent anyone from benefiting).

National defence, lighthouses and street lighting are classic examples. Because no one can be

excluded from enjoying a public good, private markets have little incentive to supply it—free riders

would benefit without paying. Governments therefore often provide public goods and use taxes,

subsidies or regulations to address externalities. Carbon taxes, emissions trading schemes and

fuel economy standards are examples of policies aimed at internalising the social costs of

pollution; patents, R&D subsidies and public funding of research encourage innovation and other

socially beneficial activities.

Business Cycles and Economic Growth

Economies rarely grow in a straight line; instead they move through business cycles

characterised by periods of expansion and recession. The National Bureau of Economic

Research (NBER) dates these cycles for the U.S. Expansions begin at a trough and end at a peak;

recessions run from a peak to the next trough. During expansions, employment and incomes rise,

corporate earnings grow and consumer confidence is high. Eventually, imbalances like excessive

borrowing or an external shock trigger a downturn. Recessions are typically shorter than

expansions—since World War II the average U.S. expansion has lasted about five years, while the

average recession has lasted about eleven months. However, their impact can be severe, as seen in

the Great Recession of 2008–09 and the short but sharp pandemic recession of 2020.

The longest U.S. expansion on record stretched 128 months from June 2009 to February 2020. It

ended abruptly when the pandemic struck, causing output to contract at a historic pace. Recessions

occur regularly in other countries as well; they may result from financial crises, oil price shocks,

political instability or natural disasters. Policymakers use monetary and fiscal tools to smooth

cycles—cutting interest rates, increasing government spending or reducing taxes in downturns and

reversing these measures when growth is strong. In the long run, productivity gains from

technological advances and investments in education and infrastructure are the primary drivers of

economic growth.