History offers powerful lessons about how financial markets and the

broader economy behave under stress. The following case studies

highlight major events that shaped recent economic history and

provide context for concepts you’ll encounter elsewhere on this

site.

The 2008–09 Financial Crisis

In the years leading up to 2007, home prices in the United States

more than doubled as low interest rates and new mortgage products

made borrowing easy. Lenders extended credit to many

borrowers with weak credit histories, and these subprime

mortgages were bundled into complex securities sold around the

world. When housing prices peaked in 2006 and began to fall,

defaults on mortgage loans jumped. Financial institutions

holding mortgage‑backed securities suffered heavy losses, and

credit markets seized as investors lost confidence. Several

large investment banks either failed or required emergency

bailouts. The U.S. economy entered a deep recession known as

the “Great Recession,” and unemployment rose sharply. The

Federal Reserve responded with unprecedented actions to provide

liquidity and cut interest rates to near zero, while Congress

passed major reforms to strengthen financial regulation. The

recovery began in mid‑2009 but was the slowest in decades, and

the crisis reshaped global banking and regulatory policy.

The 2020 COVID‑19 Recession

In March 2020, the outbreak of COVID‑19 and stay‑at‑home

restrictions triggered the sharpest economic contraction on

record. Businesses closed and consumers stayed home, causing

a sudden collapse in spending. The unemployment rate in the

United States jumped to 14.7 percent in April 2020, while real

GDP per capita fell at an annualized rate of nearly 25 percent.

Unlike the Great Recession, there was nothing fundamentally

wrong with the economy; it was a public health crisis that

forced production to halt. The Federal Reserve slashed

interest rates, launched emergency lending programs and

supported credit markets. Congress passed multiple stimulus

packages to help households and businesses. Once vaccines

rolled out and restrictions eased, economic activity rebounded

quickly, although the recovery has been uneven across sectors.

The 2021–22 Inflation Surge

After the pandemic recession, prices began rising rapidly as

supply chains struggled to keep up with surging demand.

Disruptions at ports, factories and logistics providers

created shortages and backlogs of goods, particularly cars and

consumer electronics. Energy prices swung wildly, with oil

and natural gas costs soaring as economies reopened and

geopolitical tensions disrupted supply. At the same time, the

U.S. labor market tightened; job openings far exceeded the

number of unemployed workers, pushing wages higher. Economists

identified three main drivers of post‑2020 inflation: volatile

energy prices, supply‑chain bottlenecks and elevated

automobile prices. These factors pushed headline inflation

well above the Federal Reserve’s 2 percent target in 2021 and

2022. While some price pressures have eased, the episode

underscored how both demand and supply shocks can feed

inflation.

Federal Reserve Rate Hikes (2022–23)

To bring inflation back toward its 2 percent goal, the Federal

Open Market Committee (FOMC) embarked on its most aggressive

tightening cycle in decades. Beginning in March 2022, the

FOMC raised the target range for the federal funds rate at

every meeting through May 2023. The first hike was a modest

0.25‑percentage‑point increase, but subsequent moves were

larger—four straight 0.75‑point increases in June, July,

September and November 2022. By June 2023 the target range

reached 5 to 5¼ percent, the highest in years. Policymakers

acted quickly because inflation was persistently elevated and

the labor market remained very tight, and they sought to

demonstrate their commitment to price stability. After mid‑

2023 the pace of increases slowed as the cumulative effects of

earlier hikes and banking stress began to restrain activity.

The Student Loan Debt Burden

Higher education in the United States is increasingly financed

through loans. As of early 2026, Americans owed roughly

$1.8 trillion in student loans. Federal loans accounted for

about 91 percent of this debt, with private loans making up

the rest. More than 42 million people hold federal student

loan debt, and the average balance is close to $40,000. Many

borrowers incur even larger balances for graduate and

professional degrees. Rising tuition costs and slow wage

growth mean that paying down student debt can take years.

Policymakers debate how best to address this burden, with

proposals ranging from enhanced loan forgiveness to expanded

grant aid and tuition reforms. For students, it’s crucial to

borrow only what is necessary and to understand the long‑term

implications of taking on large debts.

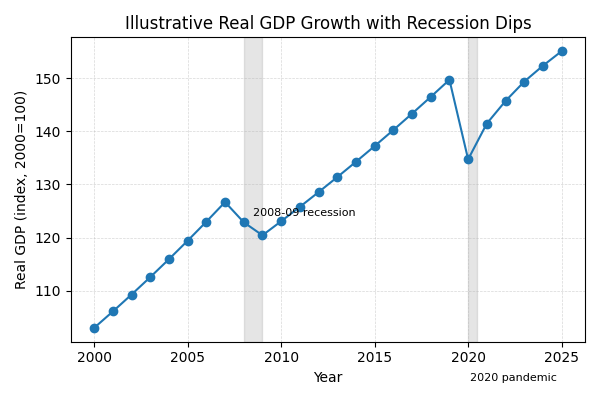

Visualizing Economic Shocks

The chart below illustrates how real gross domestic product

(GDP) growth has fluctuated over the past two decades. Notice

the sharp contraction during the 2008–09 financial crisis and

the even steeper drop in 2020 when the pandemic hit. Such

visuals help connect economic theory with real outcomes.