Investing allows your money to grow over time and helps you

achieve long‑term goals such as funding education, buying

a home or building a comfortable retirement. Simply

keeping cash under the mattress causes its value to shrink

as inflation erodes purchasing power. By purchasing

assets—stocks, bonds, real estate and others—you can

harness compound growth and potentially earn returns

that outpace inflation. However, investing always

involves balancing risk and reward: higher

potential returns usually come with greater risk. Stock

markets can rise quickly but also lose value; lower‑risk

assets like savings accounts and government bonds preserve

principal but offer modest growth. Starting early gives

compounding more time to work in your favour.

One way to manage risk is through

diversification. Spreading money across

different assets reduces the impact of any single

investment performing poorly. A classic illustration is

a street vendor who sells both sunglasses and umbrellas to

balance sunny and rainy days. Likewise, holding a mix of

stocks, bonds, real estate and cash can make your

portfolio more resilient. Diversification, along with

careful asset allocation, is central to building a

portfolio that matches your goals and risk tolerance.

Asset Allocation

Asset allocation means dividing your

investment portfolio among different categories—primarily

stocks, bonds and cash equivalents. The appropriate mix

depends on your time horizon—how long until you need

the money—and your risk tolerance—how comfortable you

are with fluctuations in value. A longer time horizon

allows you to take on more risk because you have time to

recover from market downturns, while a shorter horizon

calls for a more conservative mix.

Investors often choose among typical profiles. An

aggressive portfolio might hold 80–90 % in stocks and

the rest in bonds and cash; a moderate portfolio might

target about 60 % stocks and 40 % bonds; a

conservative portfolio might tilt toward bonds and

cash. As you approach a goal, it’s common to shift

gradually from riskier to more conservative investments—a

process called glide‑path investing. Periodically

rebalancing your portfolio back to your target allocation

keeps you from becoming overexposed to one asset class.

Types of Investments

Stocks: When you buy shares in a company you

become a part owner and are entitled to a portion of its

earnings. Over long periods stocks have delivered the

highest average returns because shareholders participate

directly in corporate profits and growth. Stock prices

can swing widely from year to year—rising sharply during

booms and plunging in downturns—which is why they’re

considered higher risk. You can invest in large‑cap or

small‑cap companies, growth or value strategies, and

domestic or international markets depending on your

preferences and goals.

Bonds: Buying a bond is essentially lending

money to a government, municipality or corporation. In

return you receive regular interest payments and the

principal back at maturity. Bonds are generally less

volatile than stocks and provide more predictable income.

Government bonds tend to be safer than corporate issues;

high‑yield (or “junk”) bonds offer higher interest rates but

come with greater risk of default. Municipal bonds can

provide tax‑advantaged income, especially if you live in

the issuing state.

Cash and Cash Equivalents: Savings accounts,

certificates of deposit (CDs) and U.S. Treasury bills fall

into this category. These are the safest assets because

your principal is protected, making them ideal for

emergency funds or short‑term goals. The trade‑off is

that they yield the lowest returns and inflation will

gradually erode their purchasing power if held for long

periods.

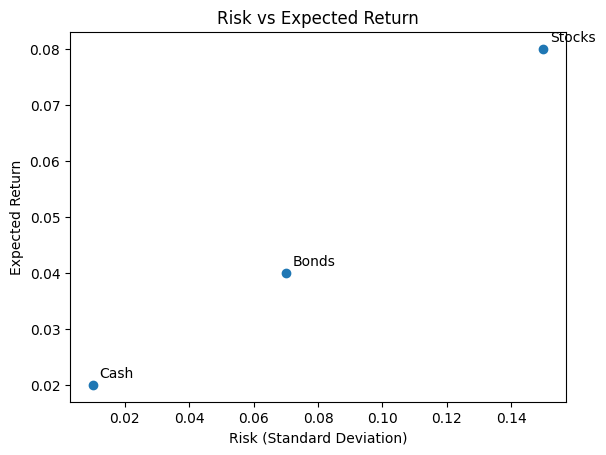

Investors must balance risk and reward. Stocks (top right)

tend to offer higher potential returns but come with

greater volatility. Bonds occupy the middle ground,

providing moderate returns with less risk. Cash and cash

equivalents (bottom left) have the lowest risk but also

the lowest expected return.

Index Funds and Exchange‑Traded Funds (ETFs)

An index fund is a type of mutual fund or

exchange‑traded fund (ETF) that seeks to track the

performance of a market index such as the S&P 500 or the

Russell 2000. Because you cannot buy an index itself,

index funds provide an indirect way to invest in all the

companies represented in the index. Many investors use

index funds to gain broad market exposure quickly and at

low cost.

Index funds may invest in all the securities of an index or

just a sampling. In market‑capitalization‑weighted

indexes, larger companies make up a bigger share of the

fund. Some index funds use derivatives like futures or

options to achieve their objective. Because index funds

follow a passive investing strategy and trade

infrequently, they often have lower fees than actively

managed funds and can be more tax efficient. For example,

the SPDR S&P 500 ETF (ticker symbol SPY) charges a

management fee of just a few hundredths of a percent and

gives you exposure to 500 of the largest U.S. companies.

While index funds aim to match the performance of a

benchmark, actively managed mutual funds try to beat the

market by picking specific securities. Some investors

prefer index funds for their simplicity, diversification and

low cost, while others choose active funds hoping that a

skilled manager will outperform the benchmark. Evidence

shows that over long periods, only a minority of active

funds beat comparable index funds after fees.

Mutual Funds vs. ETFs

Mutual funds and ETFs are both

pooled investment vehicles that provide diversification and

professional management. However, they differ in how

shares are bought and priced. Mutual funds sell and redeem

shares directly at the fund’s net asset value (NAV) once

per day after the market closes. ETFs trade on stock

exchanges like shares of individual companies; their price

fluctuates throughout the trading day as investors buy and

sell.

Both mutual funds and ETFs are regulated by the U.S.

Securities and Exchange Commission (SEC) and must follow

securities laws. They allow investors to gain exposure to

a broad portfolio without having to purchase individual

securities. ETFs are often used by investors who value

intraday trading, lower expense ratios and potential tax

efficiencies; however, you may pay a brokerage commission

when buying or selling shares (depending on your broker).

Mutual funds may offer more convenient features for

automatic contributions, reinvestment of dividends and

systematic withdrawals. Some mutual funds charge sales

loads or higher expense ratios, so it’s important to

compare costs.

401(k) Retirement Plans

A 401(k) plan is an employer‑sponsored retirement account

that lets you set aside part of your paycheck before income taxes

are taken out. Most plans allow you to contribute a percentage

of your salary up to an annual limit set by the Internal Revenue

Service (the limit has been in the low twenties of thousands of

dollars in recent years, with an additional catch‑up allowance

for workers age 50 or older). Many employers offer a

matching contribution on the first few percent you defer. At

a minimum, you should contribute enough to get the full match—

it’s essentially “free money” that can significantly boost your

savings.

Contributions to a traditional 401(k) reduce your current taxable

income and grow tax‑deferred; you don’t pay taxes on the money

until you withdraw it in retirement. Some employers also offer

Roth 401(k) options, where you contribute after‑tax dollars and

qualified withdrawals are tax‑free. If you withdraw money

before age 59 ½ you may owe both income tax and a 10 % early

withdrawal penalty, so these accounts are best left untouched

until retirement. Starting in your early 70s you must take

required minimum distributions (RMDs) from a traditional 401(k).

Within a 401(k), you typically select from a menu of mutual

funds and target‑date funds investing in stocks, bonds and

sometimes stable‑value funds. Review the expense ratios and

long‑term performance of the funds offered, and choose an

allocation that matches your risk tolerance and time horizon.

As you change jobs, you can roll your 401(k) balance into a

new employer’s plan or into an individual retirement account

(IRA) to maintain its tax‑advantaged status. The combination

of tax‑deferred growth, employer matching and automatic payroll

deductions makes a 401(k) one of the most effective ways to

save for retirement.