A budget is a plan for how you will spend, save and invest

your money. Begin by selecting a time period—such as a

month or school term—and listing all sources of income.

Next, track every expense: tuition and fees, textbooks,

housing, groceries, transportation, entertainment and

discretionary purchases. Compare your total spending to

your income and adjust so you live within your means.

Grouping expenses into categories like needs, wants and

savings makes it easier to see where to cut back or save

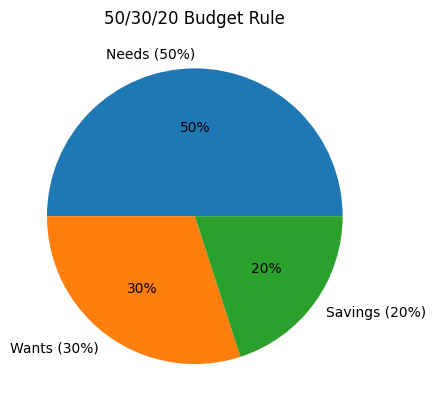

more. A popular guideline is the 50/30/20 rule: use

50 % of your income for needs, 30 % for wants and 20 % for

savings or debt repayment. Building an emergency fund to

cover three to six months of expenses can help you avoid

debt when unexpected costs arise.

The 50/30/20 rule suggests allocating roughly half of your after‑tax income to needs, 30 % to wants and 20 % to savings or debt repayment.

Compound Interest

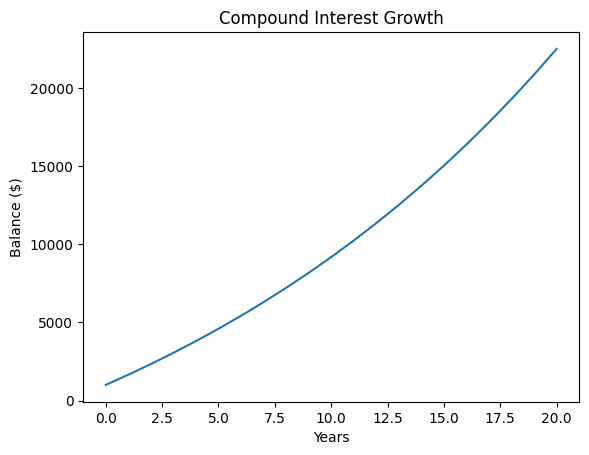

Compound interest is interest earned on both

your original principal and on the interest already credited

to your account. Because interest is added back to the

balance, future interest is calculated on a larger amount

each period. For example, if you deposit $100 at a 5 % annual

rate, you’ll have $105 after one year and $110.25 after two

years because you earn interest on the $5 from the first

year. Over decades, compound growth can dramatically

increase your savings. Starting early is powerful: someone who

invests $1,000 at age 18 and contributes $50 every month at

5 % could have more than $20,000 by age 40. Even small

contributions add up quickly when earnings are added to

prior interest.

Illustration of compound growth: with a starting principal of $1,000 and modest annual contributions, the balance grows steadily over 20 years as interest is earned on both principal and accumulated interest.

Credit Scores

Your credit score is a three‑digit number that

helps lenders gauge how likely you are to repay a loan. In

the U.S., most scores range from 300 to 850; the higher

your score, the easier it is to qualify for credit and the

lower the interest rate you’re likely to be offered. Credit

scores are calculated from the information in your credit

reports, including payment history, outstanding balances,

the length of your credit history, new credit applications

and the mix of credit you use. To improve your score,

pay all bills on time, keep credit card balances well

below their limits, maintain older accounts to lengthen

your credit history and review your reports regularly for

errors or fraud. You can request a free credit report

from each of the major credit bureaus once every 12

months through AnnualCreditReport.com.

Student Loans

Many students rely on federal loans to pay for college and

graduate school. Direct Subsidized Loans are based on

financial need; the government pays the interest while you

are in school at least half‑time, during the grace period

and during deferment. Direct Unsubsidized Loans are

available to undergraduate and graduate students regardless

of need, but interest accrues from the time the loan is

disbursed. Private student loans typically have higher

interest rates and fewer borrower protections. To reduce

the total cost of your loan, try to pay the interest

as it accrues, make extra payments when possible and

consider scholarships, grants and work‑study programmes to

borrow less.

Roth IRA

A Roth IRA is an individual retirement

arrangement funded with after‑tax dollars. Unlike

traditional IRAs or 401(k)s, contributions to a Roth are

not tax‑deductible, but any earnings and qualified

withdrawals are tax‑free. Because you pay taxes up front,

a Roth can be especially beneficial if you expect to be in

a higher tax bracket in retirement. There is an annual

contribution limit (several thousand dollars) that depends

on your age and income. You can withdraw your

contributions (but not earnings) at any time without

penalty, and Roth IRAs have no required minimum

distributions in retirement.

401(k) Plans

Many employers offer 401(k) plans, a type of

defined‑contribution retirement account that lets you defer

part of your salary into an individual account before

income taxes are taken out. Employers often match a

portion of your contributions—commonly 3 % to 5 % of

your pay—which is essentially free money. The IRS sets a

yearly limit on how much you can contribute, and your

contributions plus earnings grow tax‑deferred until you

withdraw them in retirement. Participants choose the

investments in their accounts, typically from menus of

stock, bond and money‑market funds. Starting early and

contributing enough to get the full employer match can

significantly boost your savings. However, withdrawals

before age 59½ generally trigger taxes and a penalty, so

401(k) funds are best left untouched until retirement. Be

sure to understand your plan’s vesting schedule, fees and

investment options so you can make informed choices.

Inflation and Purchasing Power

Inflation reduces the purchasing power of money: as

prices rise, each dollar buys fewer goods and services.

The U.S. Consumer Price Index, which measures the cost of

a basket of typical purchases, surged in 2021–2022 as

supply‑chain disruptions and energy price spikes pushed

inflation to multi‑decade highs. To stay ahead of

inflation and preserve your standard of living, it’s

important to save and invest so your money grows faster

than prices rise. Investing in diversified stocks, bonds

and other assets can help your portfolio outpace

inflation over the long term.